What is the Role of Customer-Facing Sales Frontends in Non-Life Insurance Products?

Written by Danubius IT Solutions

Far from being merely aesthetic digital interfaces, customer-facing sales platforms are instrumental in bridging the gap between insurance providers and customers.

They are transforming the presentation, understanding, and purchase process of insurance products, marking a pivotal point in the trends shaping customer experience.

This shift also underscores the industry-wide challenge: of navigating legal and regulatory compliance while modernizing legacy systems to remain competitive in a dynamically changing market.

Embracing Digital Transformation

In addressing the digital transformation objectives of insurers, it's essential to recognize the widespread challenges they face, from adhering to legal and regulatory mandates to modernizing legacy systems amid constant market shifts.

Whereas the rise of InsurTech startups has simplified the online process of finding and purchasing insurance, it presents new challenges for traditional insurers to adapt their strategies. Success in this evolving environment hinges on anticipating and embracing change, particularly in the realm of digitalization.

Insurance companies also approach the implementation of digitalization at a varied pace, as it is not just a modernization and a uniform sprint towards cloud adoption but a tailored strategy to bolster customer interaction and operational efficiency. Shifting gears on digitalization is becoming an increasingly growing pressure. As a result, the old paper-based regulations, processes, and behaviors are finally disappearing and have given way to much easier and faster solutions, such as remote identification, digital signatures, as well as other collaboration tools, which are usually built on outdated backend systems.

An Overview of Non-Life Insurance Products

To give you an example that fosters understanding, the US insurance industry of non-life products experienced a significant underwriting loss in Q1 2023, which was the largest in 12 years. Factors contributing to this include soaring construction and contractor service costs, increased frequency of natural disasters, and rising property-catastrophe reinsurance costs.

Insurers are grappling with balancing rising expenses and customer expectations, which has led to higher insurance rates across various sectors, including commercial property and car insurance.

Given the economic landscape, insurance premiums increased in 2023 and are still expected to rise in 2024, driven not directly by insurance rate hikes but by broader inflation and rising service costs. This scenario nudges insurers towards innovative product offerings to retain customer engagement amidst financial pressures. Notably, insurers are exploring:

-

Modular Policies: Customizable insurance coverage allowing customers to select and pay for only what they need, enhancing flexibility and affordability.

-

Event-Based Insurance: Temporary coverage activated by specific events, offering targeted protection without long-term commitment, appealing to consumers seeking cost-effective, situational insurance solutions.

These adaptations aim to align insurance products more closely with consumer needs and economic realities, ensuring that insurance remains accessible and relevant.

As we can see, the industry faces a transformative phase, with insurers exploring new models like embedded insurance and parametric insurance, which offer innovative coverage options based on specific events or indices.

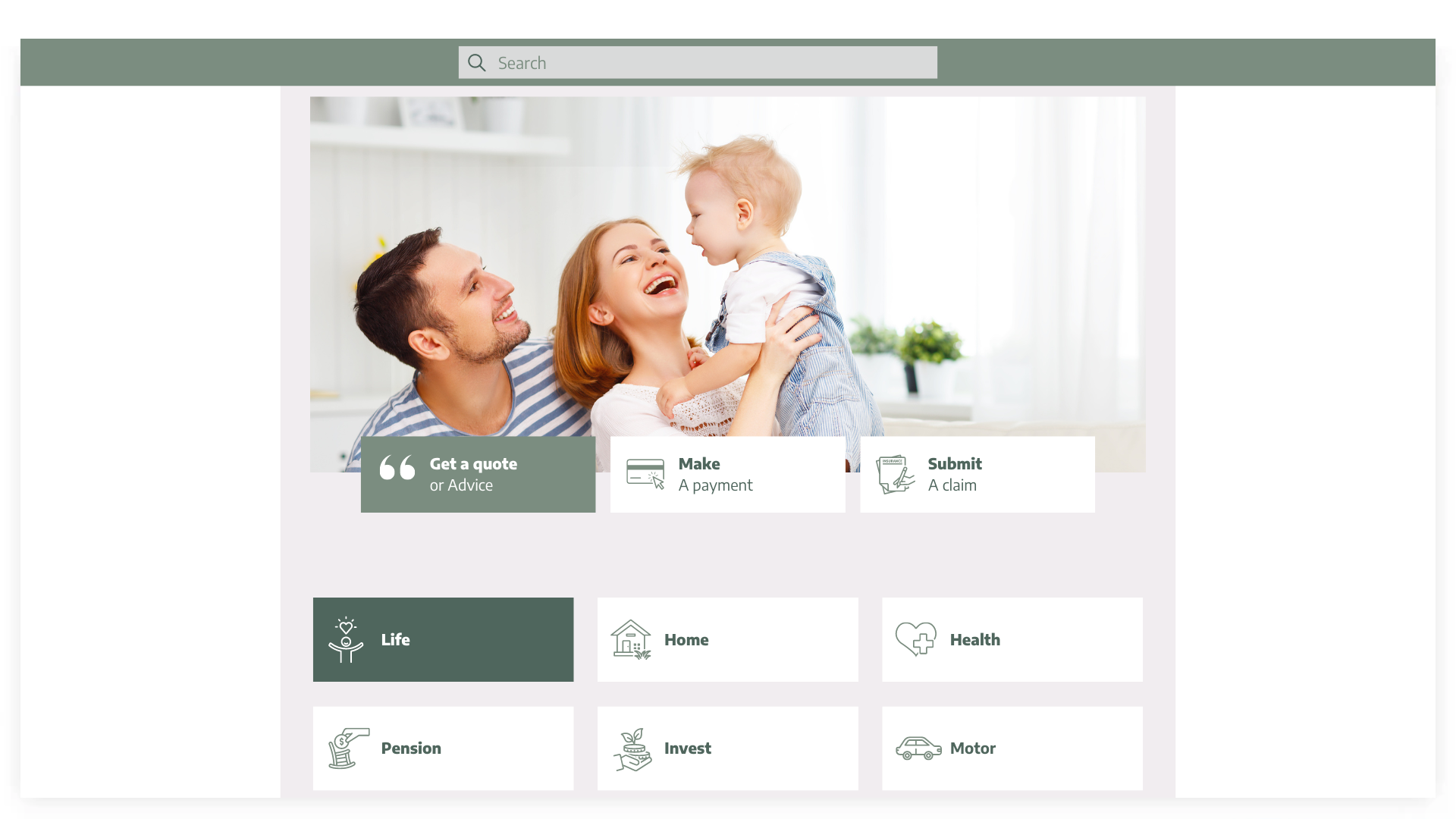

Enhancing Customer Experience with Customer-Facing Sales Frontends

Redefining the role of customer-facing sales frontends is crucial, especially given the increasing complexity and rising costs of non-life insurance products.

These interfaces have become some of the most important sales channels that are pivotal in enhancing user engagement. The key is a clean, quick, and easy-to-use interface that helps customers find their way around the products:

-

Replacing lengthy product descriptions with visual elements like pictorial illustrations and video tutorials can significantly clarify offerings.

-

Simplification is key; offering pre-set product packages instead of overwhelming options can streamline the decision-making process.

-

Additionally, ensuring that these interfaces are mobile-friendly and easy to navigate is essential in catering to the modern consumer's expectations and needs.

Ultimately, these innovations are not just about aesthetic appeal but about making insurance more accessible and user-friendly. As consumer behavior is shifting due to cost concerns, providing clear, accessible information and simplifying the purchasing process can help make informed decisions and maintain customer trust.

Driving Sales and Revenue

The digital insurance industry is growing rapidly, with a current global market CAGR of 10.80%.

Key trends – such as automation and a data-driven approach – drive this growth, impacting how insurance products are sold and managed.

Automation, particularly in underwriting and claims processing, is transforming these areas by reducing human involvement and streamlining processes. This saves time and costs for insurers and also enhances customer experience due to quicker processing times.

The implementation of omnichannel approach promises to provide a seamless customer experience across multiple channels. For example, if a customer begins calculating an insurance premium online but doesn't complete the process, the call center can see this activity. At this point, they might reach out to offer assistance, suggesting adjustments to the quote if necessary, thereby enhancing customer engagement and satisfaction.

Furthermore, leveraging online marketing strategies opens numerous opportunities for insurers, significantly boosting customer acquisition rates. By targeting specific demographics through social media and other digital platforms, insurers can reach and engage with potential clients more effectively than ever before.

Additionally, optimizing websites to convert visitors into clients is crucial. A professional, easy-to-navigate website with engaging content can significantly increase traffic and sales. Incorporating video marketing can also enhance brand trust and increase conversions.

This approach helps in reaching customers via such various channels while maintaining consistent service quality. Additionally, the growing adoption of customer self-service models, accelerated by the pandemic, has opened up new avenues for sales and service.

Self-service portals and mobile applications are increasingly preferred by tech-savvy consumers, allowing them to purchase and manage insurance products conveniently. Such digital transformations are key to driving sales and revenue in the sector today.

Technology Background is Vital

Integration with backend systems is of course essential for the frontends’ effectiveness, however, insurers currently rely on outdated legacy systems for backend and middleware, so transitioning to more modern infrastructure is crucial. Persisting with these legacy systems hampers the ability to keep pace with rapid technological advancements, leading to several potential drawbacks.

Firstly, it restricts the agility needed for risk assessment and pricing, impacting customer service quality. Additionally, it limits the effective use of AI and ML for analyzing large datasets, which is increasingly vital for optimizing operations and enhancing decision-making processes. Upgrading these systems is essential if an insurance company wants to ensure sustainability and maintain competitiveness.

Such technologies allow insurers to automate routine tasks, improve underwriting processes, and predict risks more accurately. As this move towards a more integrated, technology-enabled approach also involves a shift in how insurers operate and interact with customers, it is clear that the integration points beyond the need of simply digitizing operations; it is a choice that’s vital for insurers in their goal of remaining competitive.

Security and Compliance

In this context, the insurance industry faces quite the challenges due to the vast amounts of sensitive personal and financial data they handle.

Cybersecurity is a growing concern, with insurers being prime targets for cyber-attacks due to the nature of the data they collect. The global financial costs of data breaches are substantial; it averaged around €4 million in 2023 (which was the result of a 15% increase over 3 years), but the impact on brand reputation and customer trust is equally significant.

Insurers are thus focusing on proactive measures to prevent and mitigate cyber-attacks. In addition to technical safeguards, there is also an increasing emphasis on compliance with regulatory standards to protect sensitive customer data.

However, as in all other industries, increased cybersecurity and compliance in digital insurance are essential both for safeguarding and maintaining customer trust and confidence.

The Future of Digitalized Insurance

The trend of common service layers and microservice architecture development has the most transformative effect on the insurance industry, as it enables efficient building on robust legacy systems as well as the effective integration of modern services. Their evolution provides a robust foundation for digital products, enabling real-time delivery and facilitating a variety of front-end solutions.

Specifically, these technologies empower insurers to deploy and manage digital services more efficiently, allowing for rapid adaptation to market changes and customer needs. By leveraging both common service layers and microservices, insurance providers can offer personalized, on-demand services, enhancing customer experience and operational agility.

Moreover, this approach streamlines the development and deployment of new insurance products while significantly reducing time-to-market, setting the stage for a more dynamic, customer-centric insurance industry.

And last but not least, the expansion of digital channels signifies a paradigm shift from traditional physical sales channels to more dynamic, digital mediums. Such a new outlook aligns with the growing customer preference for self-service options and digital engagement while insurers are leveraging digital tools such as chatbots and virtual assistants to meet evolving customer demands, thus enhancing the overall customer experience.

Conclusion

All in all, customer-facing sales frontends in non-life insurance are a critical component in the customer journey, enhancing experience, driving sales, and building lasting and loyal relationships.

And remember, your peace of mind is just a click away. Discover the edge that Danubius can deliver to non-life insurance products and services with customer-centric digital solutions: whether it’s modernizing legacy systems or deploying cutting-edge technologies, we ensure seamless integration, enhanced security, and engaging customer experience.

Interested in IT solutions tailored to your business? Contact us for a free consultation, where we'll collaboratively explore your needs and our methodologies.